Great-Britain – Continental Europe and Nordics

Linking the markets of Great Britain with Continental Europe and the Nordic region.

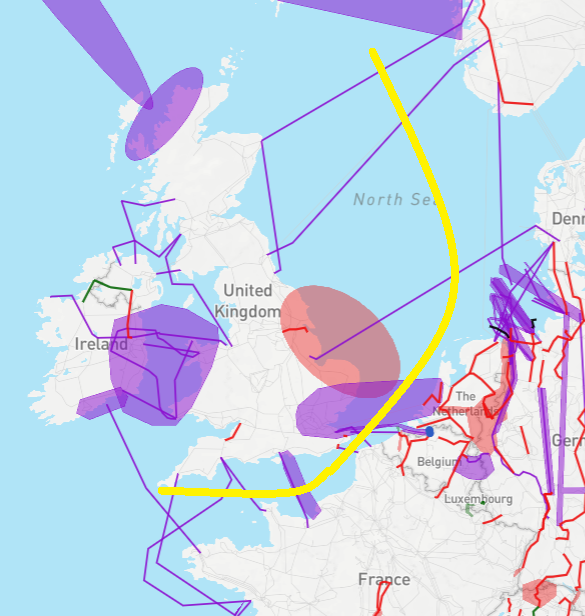

The generation shift from coal to gas and from thermal to renewables is the main driver for increasing interconnection capacity between the different systems making up the North Sea region. Integrating the British system towards both the Continental and the hydro-based Nordic system, allows benefiting from the complementariness between their generation mix structures. Hence, developing new interconnections across this boundary is important to achieve the desired European market integration as well the integration of renewable energy, preparing for a power system with lower CO2-emissions for most of the Visions. Investments in the boundary play a key role in developing the Northern Seas Offshore Grid Infrastructure and will improve security of supply in the whole region, e.g. during times of low wind, high demand, dry years. In addition, HVDC projects in particular add flexibility to the systems due their controllability.

TYNDP findings

The analyses show that projects between the Nordic and British systems do have high benefits, however there are also high costs due to the long distances. Substantial price differences remain bween the Continental and British systems depending on the Vision.

In gas before coal market conditions, projects between the systems lead to decreased CO2-emissions. However, in visions with low CO2-prices where coal is cheaper than gas as e.g. in Vision 1, the projects may lead to an increased coal-fired production and subsequently increased CO2-emissions.

Welfare and Capacity

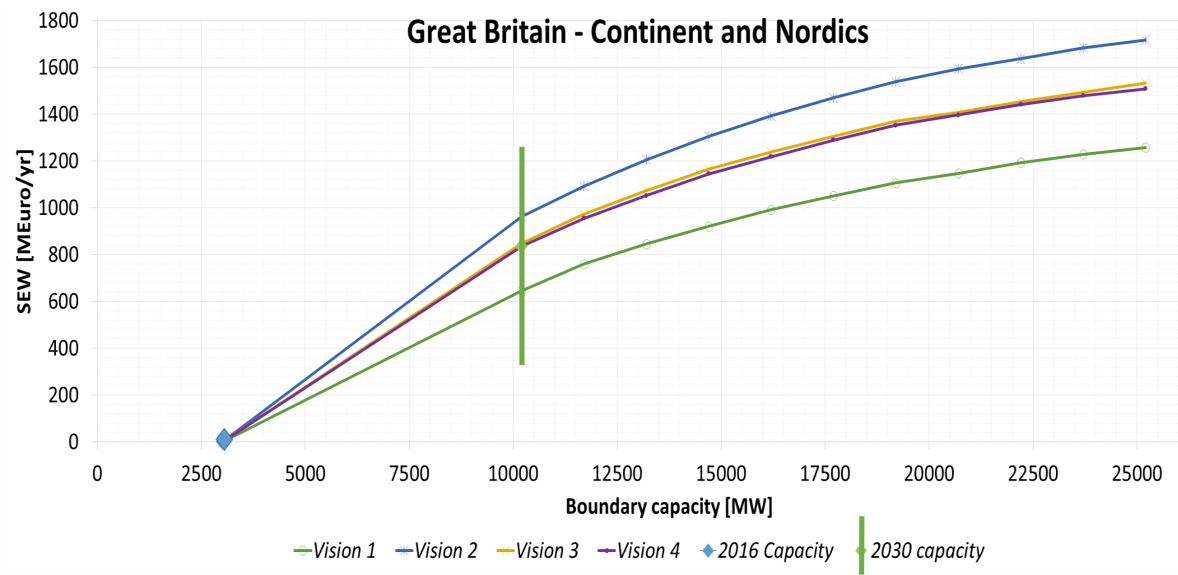

Market based capacity analysis performed in the TYNDP 2016 shows a significant potential for increasing the capacity between the British, Nordic and Continental systems. At the same time, it is important to pay attention to the scenario assumptions. Bringing CO2, oil , gas, coal prices down to 2016 level will influence the SEW values in a negative direction. The SEW values would be smaller than the values identified for 2030. The CO2 price assumptions for 2030 are higher than the ones seen today. Higher CO2 prices create larger marginal cost price differences between the different generation technologies. Having a look at the SEW related to increasing boundary capacity, the values of the different visions indicates that fuel mix is the main driver for price differences hence they drive the SEW-values.

Great Britain is a net importer, mainly from the continent, in both Visions 1 and 2, but less in Vision 2 given the higher amount of offshore wind in GB in that scenario. In the greener Visions 3 and 4, Great Britain turns into a net exporter, mainly to the continent. This is mainly caused by the different fuel mix in GB as compared to the continent. The main driver for the lower prices in GB in Visions 3 and 4 is the relatively large share of gas fired generation in GB.

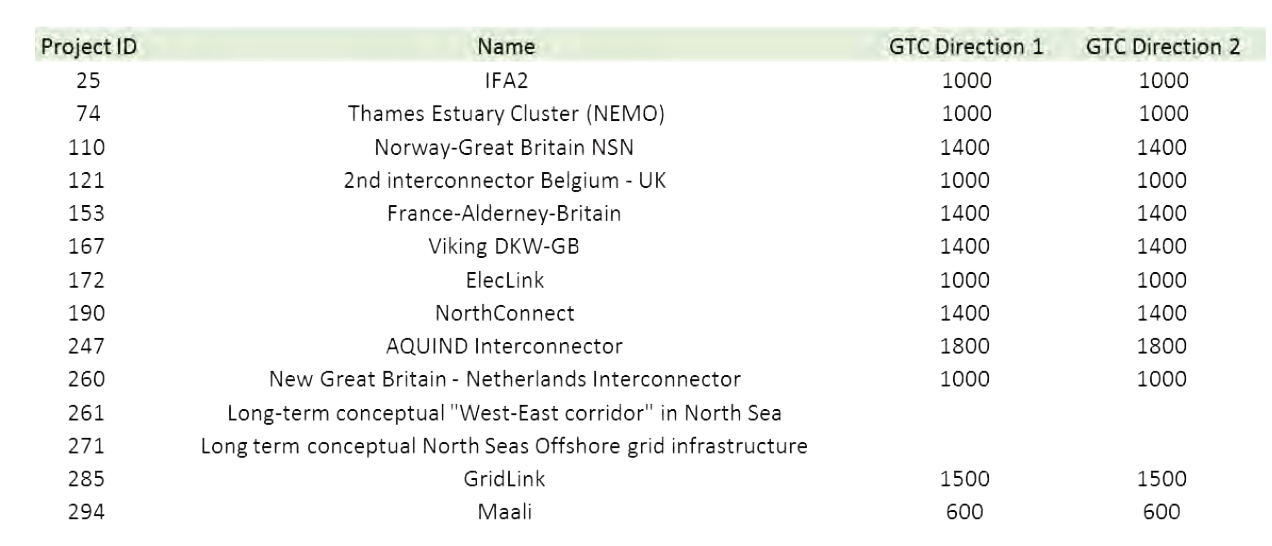

Today’s capacity across the boundary is 3GW (blue dot), while the reference capacity for 2030, including all TYNDP 2016 mid-term and long-term projects, is about 10 GW (green vertical line). Projects not being part of the reference capacity, usually less mature projects or those being built beyond 2030 are indicated on the right hand side of the green vertical line.

Interconnection target for 2030

Making the balance between social welfare gain and infrastructure investment costs for higher levels of interconnection, the level of interconnection is above 10 GW for all Visions. The present and planned investments show that the reference capacity might be reached by 2030, even though this includes projects of more than 7 GW.